Stock Market The Week Ahead: Geopolitics Takes Center Stage

[ad_1]

posteriori/iStock via Getty Images

Geopolitics ruled markets last week as Russia continues to maintain a growing military presence along the Ukrainian border, while President Biden sounds an ever-heightening alarm about the consequences of an invasion. As a result, investors continue to shed risk. An invasion will undoubtedly lead to a sharp spike in oil prices over $100/barrel, a rally in the safe havens of gold and Treasuries, and a decline in long-term interest rates. Yet similar events have rarely had a long-term impact on markets, and I don’t think this one will be any different. If a retest of the January low in the S&P 500 results from an invasion, I will view it as another buying opportunity in quality and value, which is what continues to lead in performance in 2022. Ultimately, investors will refocus on inflation and Fed policy, which is what’s dictating the longer-term trends in markets.

edwardjones.com

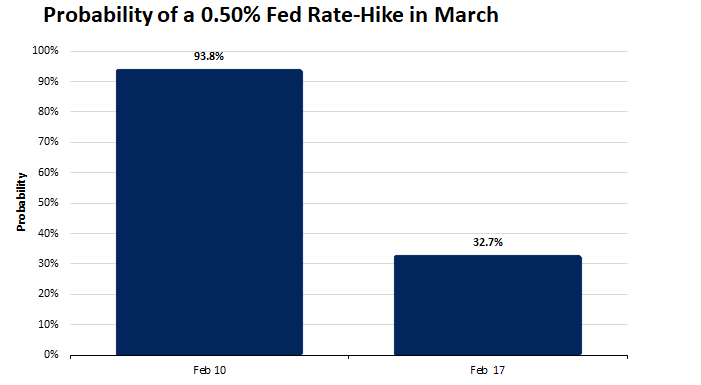

The release of the Fed’s January meeting minutes last week reduced the probabilities of a 50-basis point rate hike at the March meeting, easing fears of a more hawkish policy move. I’m still convinced that the Fed will hike by 25-basis points at each of its next three meetings, resulting in a short-term rate of 0.75% by the end of June. At that point, additional moves will be data dependent. The rate of inflation will have tapered from its recent highs, allowing the Fed to take a more measured response to tightening short-term rates. Five to six hikes that result in a rate of 1.25-1.50% by year end seems most likely to me.

edwardjones.com

That process should not derail the economic expansion or the bull market that began in 2020. Retail sales rose a solid 3.9% in January, as consumers begin to shift spending from goods to services with the rapid decline in daily new cases of COVID-19. That should accelerate further with warmer weather, the easing of economic restrictions, and the continued reopening of the economy.

The greatest concern for investors today is the 40-year high in inflation, which surpassed 7% in December to reach 7.5% in January. I spent the early part of 2021 refuting Chairman Powell’s claim that the coming inflation, which he and the Fed grossly underestimated would be transitory. A year later I’m arguing that the current rate is unsustainable, and my logic is simple. I surmise that better than half the increase of 7.5% is a function of temporary factors related to the pandemic. Some of those factors are due to the limited availability of materials, while others are due to excessive levels of stimulus-induced demand.

The supply side of the equation should be remedied by the easing and eventual end of the pandemic, while the demand side will be addressed as the savings rate falls to more normal levels and stimulus payments to consumers fade in the rear-view mirror. In both cases, we will revert to the pre-pandemic levels of economic activity. The one aspect of the post-pandemic period that will likely…

[ad_2]

Read More: Stock Market The Week Ahead: Geopolitics Takes Center Stage